💥New Chapter 11 Bankruptcy - BurgerFi International, Inc. ($BFI)💥

💥New Chapter 11 Bankruptcy - BurgerFi International, Inc. ($BFI)💥

Better burger concept and premium-casual pizza brand files chapter 11 cases

On September 11, 2024, Florida-based BurgerFi International Inc. ($BFI) and 114 affiliates (collectively, the “debtors”) filed chapter 11 cases in the District of Delaware (Judge Goldblatt). The debtors and their affiliates develop, operate and franchise BurgerFi and Anthony’s Coal Fired Pizza (“Anthony’s”) restaurants. BurgerFi provides a fast-casual, “better burger” experience while purportedly using all-natural, high-quality ingredients, while Anthony’s supposedly provides a premium-casual pizza dining experience using fresh, never frozen, high-quality ingredients.

Is it just us or has the better burger fad gotten out of hand? Don’t get us wrong we love variety, but how many different ways are there to assemble some ground beef, veggies, and cheese? Five Guys, Shake Shack, Smashburger, Bareburger, Wahlburger (yes, from Mark Wahlberg) — the choices are endless.

So we’re not surprised one of these has now hit rock bottom, and of course it’s the one that was a deSPAC, lol.

BFI currently sports 91 BurgerFi locations (76 franchised, 17 corporate-owned) and 51 Anthony’s locations (1 franchised and 50 corporate-owned). At the time of the deSPAC, BFI consisted of only the BurgerFi segment. After BFI listed on Nasdaq in ‘21 through a SPAC merger with Opes Acquisition Corp. (sponsor: Axis Capital Management), BFI went and acquired Anthony’s for $156.6mm:

“BFI acquired Anthony's in 2021 after it completed its de-SPAC transaction. As part of that merger, BFI became a borrower under the Senior Credit Facility, obligating itself to over $50 million in debt.”

Impeccable timing guys! Fast forward to ‘23 and macroeconomic factors caused the debtors’ sales to decline across both BurgerFi and Anthony’s. FY’23 revenues declined by $8.6mm and corporate-owned average sales per restaurant declined from $167k to $161k between FY’22 and FY’23.

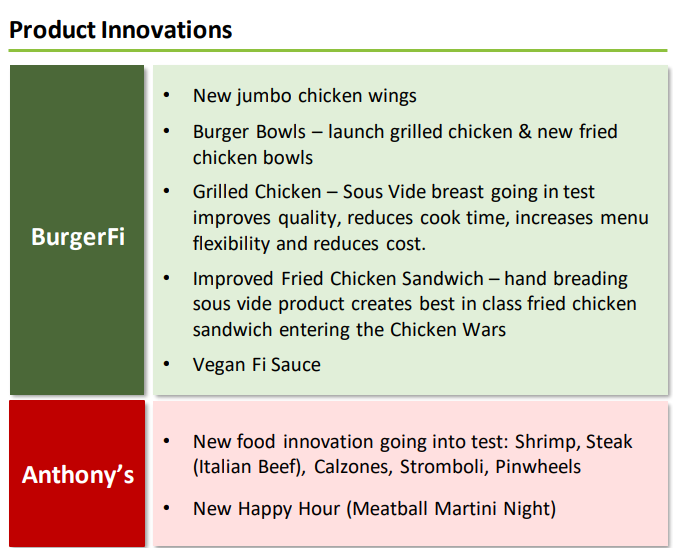

Management made several efforts to fix operations … a key strategy was, well, “new jumbo chicken wings” …

… so, uh, good job guys. Seriously, what the f*ck is a Meatball Martini? Is it meatballs + martinis or is it a meatball flavored martini? Who’s the target audience here? Middle aged Italian moms? Color us stupefied.

And of course there’s also a Beyond Meat burger!

Absent a viable turnaround plan, cash declined from $11.9mm at the end of FY’22 to $7.6mm at the end of FY’23. As of the petition date, the debtors only had $1.6mm of cash on hand. The abrupt decrease in cash caused several breaches of the minimum liquidity covenant under the senior credit facility, necessitating a May ‘24 forbearance agreement with the senior lenders.

Under the forbearance agreement, BFI agreed to run a sales process with the help of Kroll Securities Inc.** The prepetition lenders even extended $4mm of additional funds to facilitate the process.*** In addition, the debtors obtained an additional $2.5mm from their senior lender, TREW Capital Management Private Credit 2, LLC (“TREW”), as an “Emergency Protective Advance” on August 9, 2204, at which point the lenders imposed a deadline of August 28, 2024, on the debtors to obtain an LOI indicating a deal for proceeds to cover the outstanding senior secured credit facility in full ($60.3mm).****

Spoiler alert: the debtors failed to obtain an LOI. And bankruptcy!

So, what’s the goal here? The debtors are, given the pre-petition sale process, holding out hope that a buyer will emerge:

“In light of the outcome of that sales process, the Debtors are preparing proposed bid procedures and stalking horse asset purchase agreements which we are optimistic will be filed with the Court shortly.”

PETITION Note: As of the time of this writing (September 17, 2024), they are not yet on file.

The debtors intend to fund their post-petition marketing process with TREW’s backing. TREW committed to provide $5.18mm in new money along with a $10.36mm roll-up of the senior secured facility.***** The DIP carries a 12.5% PIK interest rate, a $100k origination fee, and a 2% exit fee.

The debtors are represented by Raines Feldman Littrell LLP (Thomas Francella Jr., David Forsh, Hamid Rafatjoo, Robert Marticello, Carollynn Callari) as legal counsel, Force 10 Partners (Jeremy Rosenthal, Nick Rubin) as financial advisor, and the aforementioned Kroll Securities as investment banker. TREW is represented by CM Law PLLC (Mette Kurth, Lynnette Warman) as legal counsel.

*These filings only include the 67 corporate-owned locations. But apparently franchisees are pissed off. See this letter to Judge Goldblatt from a franchisee, highlights “hefty executive salaries and reimbursements” and a lack of support for franchisees.

**Not to be mistaken with the claims agent also named Kroll. Yeah, we’re also confused.

***$2mm came from TREW as the senior lender and $2mm from CP7 Warming Bag LP as the junior lender.

****Below the $60.3mm senior secured credit facility is a junior term loan of $18.1mm from and L. Catterton Fund affiliate, CP7 Warming Bag, L.P. Major equity holders include: Ophir Sternberg (17.4%), Walleye Capital LLC (13.4%), Lionheart Equities, LLC (11.2%), CG2 Capital LLC (10.6%), Lion Point Capital, LP (10.2%), and The John Rosatti Family Trust dated August 27, 2001 (9.9%).

*****$3.5mm of new money is available upon entry of an interim order and $1.68mm is available upon entry of a final order. $7mm of the roll-up will happen upon an interim order and $3.36mm will be rolled-up upon entry of a final order.

Company Professionals:

Legal: Raines Feldman Littrell LLP (Thomas Francella Jr., David Forsh, Hamid Rafatjoo, Robert Marticello, Carollynn Callari)

Independent Directors: David Gordon, Michael Epstein

Financial Advisor: Force 10 Partners (Jeremy Rosenthal, Nick Rubin, Renee Albarano)

Investment Banker: Kroll Securities Inc.

Real Estate Advisor: Hilco Real Estate LLC

Claims Agent: Stretto (Click here for free docket access)

Other Parties in Interest:

TREW Capital Management Private Credit 2 LLC

Legal: CM Law PLLC (Mette Kurth, Lynnette Warman)

CP7 Warming Bag LP

Legal: Sheppard Mullin Richter & Hampton LLP (Edward Tillinghast, Brandon Mohamad)